Market Update: 22 June 2020

Alike looking at charts with different starting points to reflect your bias, the aesthetic of COVID cases globally can also play to a bias. The flattening of the curve was on a logarithmic scale – so despite daily COVID cases reaching new highs of 180,874 globally on June 19, it still fits in the flattened curve as we play percentages. The recent spikes in cases in the US, China and now in Australia are lost in the log.

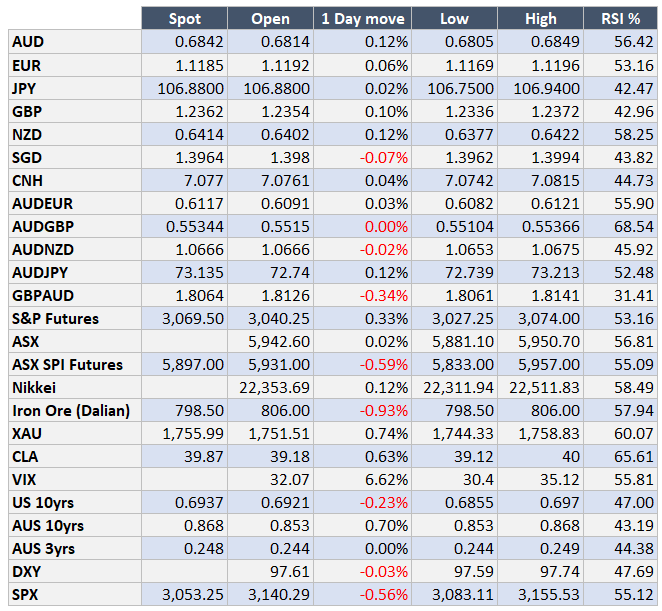

Markets are reacting to the outbreaks, but perhaps not as dramatically as you may expect. Initial reactions (generally in illiquid bouts) tend to be faded until greater participation just finds the opportunity to buy the dip. AUD initially down to 0.6805 this morning after Victoria employed a more restrictive policy due to increased cases and extending its state of emergency to July 20, Apple in the US re-closed some stores.

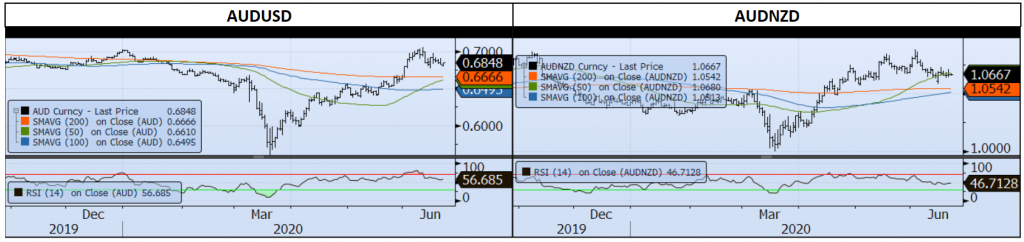

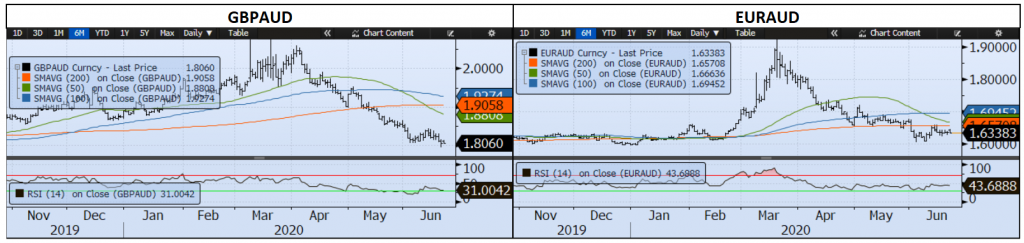

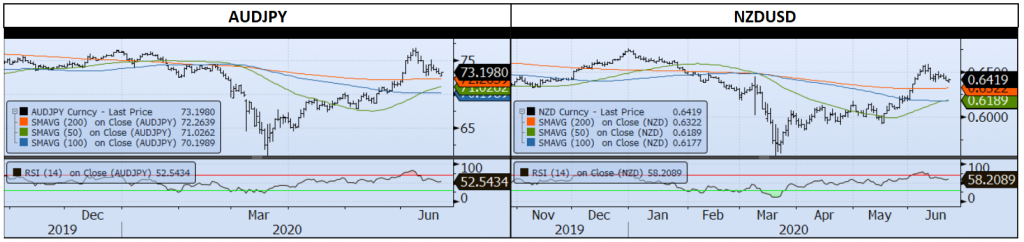

In the greater scheme of things, we would hope the outbreaks are transitory as we now know what can reduce these clusters (social distancing, monitoring, isolation etc) – as the RBA put today, “Australia went into the crisis in a better position than others”. They also would like to see AUD lower, but “we’re not a point where it’s a concern”. That’s fair to say, given some metrics have seen a correction (i.e. RSIs back from extreme levels, AUD corrected over 2c from highs).

It’s a mostly quiet start of the week, we have European PMIs and confidence whilst US home sales, PBOC and RBNZ meetings might be quite interesting – PBOC have hardly gone shock and awe so given Beijing outbreak, they might be more dovish whilst conversely, New Zealand sounded too bearish with negative rates – so a chance of a rally in NZD.

Have a great week ahead.

New COVID cases globally Daily VS Total (Logarithmic)… lot’s to see vs nothing to see here

Contact the Inside Track Research Team for more info: +61 2 8916 6115