Market Update: 3 April 2020

US Initial jobless claims reflected that mantra overnight with a whopping 6.6m claims (vs a survey of 3.7m) – double that of the prior week, the markets were pretty quick to forgive this with S&P closing up 2.3% as we head into the unknown of Non-Farm Payrolls tonight (survey of -100k sounds optimistic).

Of course it wasn’t claims that caused the rally, it was the perversity of Trump getting Russia and the Saudis to agree on cutting Oil supply causing a 25% spike higher, to settle to +15%. One would think they have no choice but to reduce supply anyway as demand wanes – not commuting to work or jumping on a plane does that.

8 weeks ago we were “lucky” to have only 15,000 cases – today we broke 1,000,000. So if we’re becoming immune to sticker shock – as that’s what happens when you close businesses, will markets become immune to how COVID-19 spreads in the next 8 weeks?.

If the global psyche is supported by the notion that we’re all suffering – so we don’t take it personally, the next question becomes for how long must we endure? This is surely the next phase of what markets will look to anticipate. A reduction in daily cases gives some light at the end of the tunnel, as does recovery rates – but it might mean less if commerce is still closed.

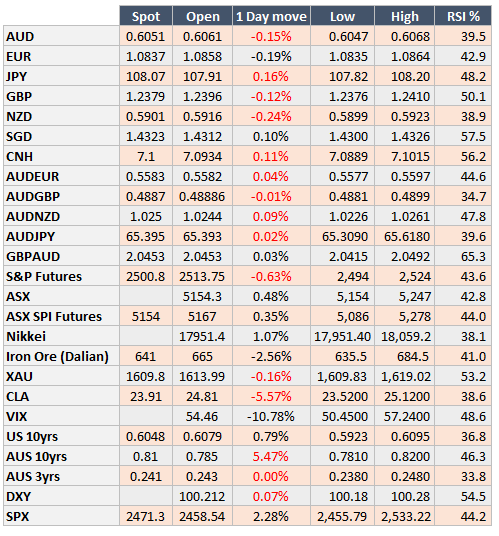

AUD feels a bit heavy.. USD does gain on Oil moves, but as well, markets don’t like things that don’t move… so if it failed above 62c, 59 might be an option.

Contact the Inside Track Research Team for more info: +61 2 8916 6115