Market Update: 7 September 2020

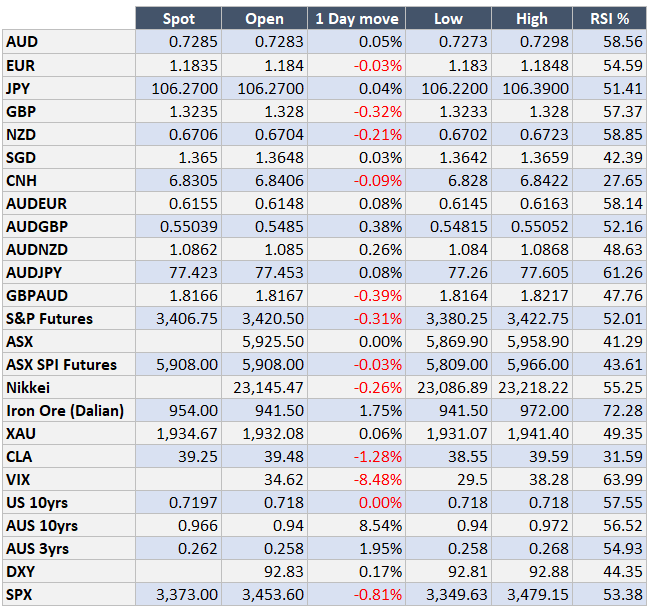

A very strong payrolls and even better drop in unemployment (8.4% vs mkt expecting 9.8%) out of the US. Even my old favourite – the participation rate showed up well. You would’ve thought S&P was more than happy to reverse the prior fall – right?

Sometimes though good news means markets reprice everything. In this instance, US 10yrs moved a quick 0.1% higher to 0.72% as maybe, just maybe the FOMC won’t be at low rates forever (just for longer). It actually was enough to cause S&P to close -0.8%. It is though fair to say the main pain went to the tech stocks in the past 2 trading sessions… falling 7.4% in total vs that of non-tech of 3.3%. It’s pretty much why ASX is close to flat on today as we don’t really sell tech!

Translate that into currencies… well USD initially rallied, then gave back ground. In a relative value sense, this data means USD should outperform and against the likes of EUR, GBP and JPY it did. It did initially against AUD and NZD but they are risk currencies so should prosper when global growth looks good – thus eventually bucked the trend.

So what is the driver? well, it would seem we have multiple drivers of this bus… but as it’s a US holiday today illiquidity will be the winner – at least until tomorrow.

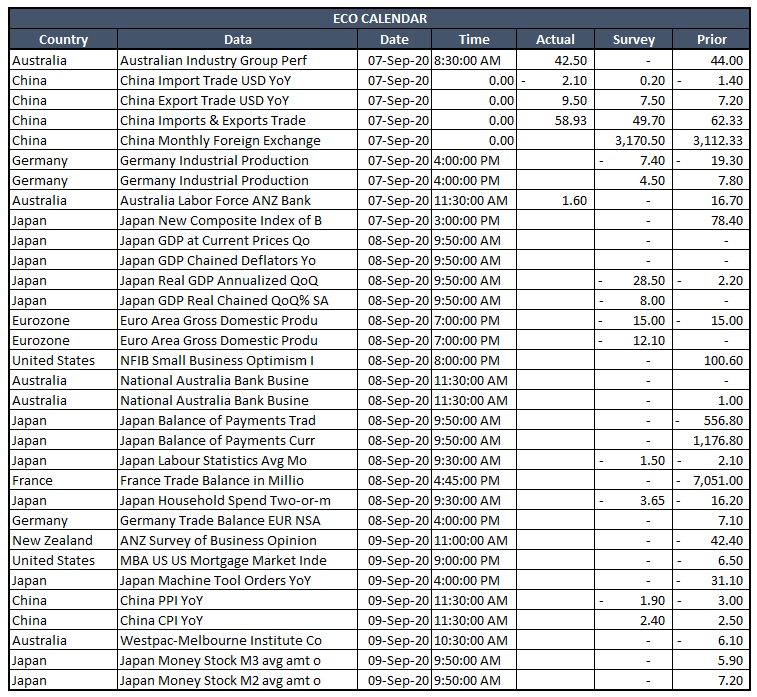

Coming up we have Japan GDP – which tends to be a snooze, but JPY fluctuations since Abe announcement have been gaining interest. Alongside this is German trade and China CPI… locally we have both Consumer and Business sentiment surveys. Victorian lockdowns won’t exactly help them.

Have a great week ahead!

Contact the Inside Track Research Team for more info: +61 2 8916 6115